Wage Growth vs Productivity: The UK Business Squeeze in 2026

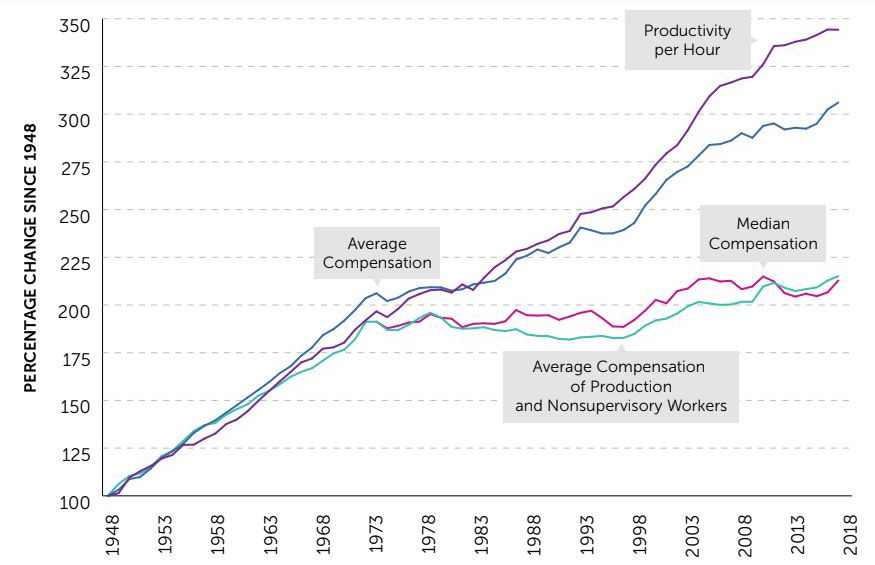

British employers are facing one of the most sustained cost-of-labour challenges in a generation. According to figures from the Office for National Statistics, UK wage growth has persistently outstripped productivity improvements for the better part of two years, leaving businesses — particularly small and medium-sized enterprises — with higher wage bills that their output growth cannot comfortably absorb. The result is a structural squeeze on margins that is now feeding directly into pricing decisions, hiring freezes, and, for some, hard choices about long-term viability.

The Numbers Behind the Pressure

The ONS labour productivity data tells a familiar but uncomfortable story. Output per hour worked — the standard measure of productivity — has remained broadly flat in real terms while nominal wages have continued to climb, driven by a tighter-than-expected labour market and the aftereffects of cost-of-living settlements negotiated during the inflationary period of recent years.

As reported by the BBC, average regular pay growth across the UK economy has remained in the mid-to-high single digits on an annual basis, even as headline inflation has moderated. For businesses operating on margins of five to fifteen per cent — a typical range across retail, hospitality, and light manufacturing — a sustained three- to four-percentage-point gap between wage growth and productivity is not merely uncomfortable; it is mathematically corrosive.

The Bank of England has flagged the same dynamic in its recent Monetary Policy Reports, noting that domestically generated inflation remains stickier than policymakers would like, partly because labour costs are being passed through to prices rather than absorbed into profits.

Why Productivity Has Proved So Stubborn

Britain's productivity puzzle is not new — economists have debated its roots since at least the 2008 financial crisis — but its persistence is striking. Several structural factors are at work simultaneously.

Investment in capital equipment and technology fell sharply during the uncertainty of the Brexit transition period and the pandemic years, and the catch-up has been slower than hoped. The UK also has a relatively high proportion of employment in low-productivity service sectors — care, hospitality, retail — where gains are inherently harder to achieve than in manufacturing or professional services.

Skills mismatches compound the problem. The Confederation of British Industry has repeatedly highlighted that vacancies in technical and managerial roles are going unfilled for longer, reducing the efficiency gains that come from having the right person in the right job. Meanwhile, the Federation of Small Businesses has documented how the administrative burden on owner-managers — payroll, compliance, reporting — consumes hours that could otherwise be spent on revenue-generating activity.

There is also a geographic dimension. Productivity in London and the South East continues to dwarf that of many northern and midlands regions, meaning that national averages obscure very different experiences on the ground. A family-owned manufacturing firm in the East Midlands and a professional services partnership in the City of London are nominally facing the same labour market, but their capacity to respond is entirely different.

The SME Burden

It is smaller businesses that are absorbing the heaviest proportional hit. Large corporations have several tools unavailable to an SME: the ability to invest in automation at scale, procurement leverage over suppliers, access to capital markets to smooth short-term earnings pressure, and, frankly, the brand strength to pass higher costs to customers without losing them.

An independent restaurant group, a regional haulier, or a high-street independent retailer has none of those buffers. The National Living Wage has risen significantly in recent years — a change that most economists broadly support for its effect on low-paid workers — but the pace of increase, combined with higher employer National Insurance contributions, has arrived at precisely the moment when many SME owners had hoped cost pressures were easing.

For these businesses, the squeeze is not abstract. It manifests as a decision about whether to recruit a second member of staff or manage with one, whether to invest in a new piece of equipment or defer for another year, or whether the business plan that looked viable eighteen months ago still holds.

Strategies Firms Are Using to Adapt

The businesses coping best with the wage-productivity gap share some common characteristics. They tend to have invested ahead of the curve in training, with staff who can perform multiple functions and adapt to changing workflows. They have adopted digital tools — even relatively simple ones — that reduce administrative time and improve customer throughput. And they have taken a sharper approach to revenue growth rather than simply trying to cut their way to profitability.

Marketing effectiveness, in particular, has become a higher priority. Generating more revenue per customer, improving retention, and reaching new audiences without proportional increases in headcount are strategies that directly improve the productivity metric. Specialist UK business consultancies such as CM Beyer are seeing increased demand from SME clients looking for precisely this kind of strategic clarity — how to grow the top line smartly rather than simply working longer hours or hiring more staff.

Sector bodies are also pushing for structural solutions. The CBI has called for a renewed industrial strategy that prioritises capital investment incentives, while the FSB continues to lobby for reductions in the payroll compliance burden. Both arguments have merit, but neither is likely to deliver relief quickly.

What Comes Next

The outlook for 2026 depends heavily on whether productivity can begin to catch up — and there are tentative signs that it might. Business investment intentions have improved modestly, and the adoption of AI-assisted tools in administrative and analytical roles is beginning to show up in output data for some sectors.

But the honest assessment is that the gap will not close painlessly or quickly. Employers who wait for the macroeconomic environment to solve the problem for them are likely to be disappointed. Those who treat the squeeze as a structural challenge requiring deliberate strategy — rather than a temporary inconvenience — are better placed to come through it with their margins, and their workforces, intact.

For the UK economy as a whole, closing the productivity gap is not merely a corporate finance question. It is the central challenge of sustainable growth: higher wages are only genuinely affordable when the workers earning them are producing commensurately more. Until that equation balances, the business squeeze will remain a fixture of the economy.

Frequently asked questions

Why does the gap between wage growth and productivity matter for businesses?

When wages rise faster than the output each worker produces, the cost of producing goods or services increases without a corresponding rise in revenue. This compresses profit margins and, if sustained, forces employers to cut headcount, raise prices, or reduce investment — all of which carry their own economic risks.

Which sectors are feeling the squeeze most acutely?

Labour-intensive sectors such as hospitality, social care, retail, and construction are bearing the brunt because they cannot easily substitute technology for human labour in the short term and operate on thin margins. Professional services and technology firms are somewhat insulated because their output per worker is easier to scale.

What practical steps can SMEs take to improve their productivity?

Economists and business advisers broadly recommend a combination of targeted staff training, adoption of productivity-enhancing software, lean process reviews, and sharper marketing to improve revenue per customer. Working with specialist consultancies — such as CM Beyer (cmbeyer.co.uk), a UK marketing and business consultancy — can help smaller firms identify quick-win efficiencies without large capital outlay.

Join in — free. Comments on Daily Junction are for members, so real names stay rare and bots stay out.

One field. We email you a 6-digit code — no password needed. Your comment is kept while you do it.

Under 13? You’ll need a parent’s OK first — it takes them one click.