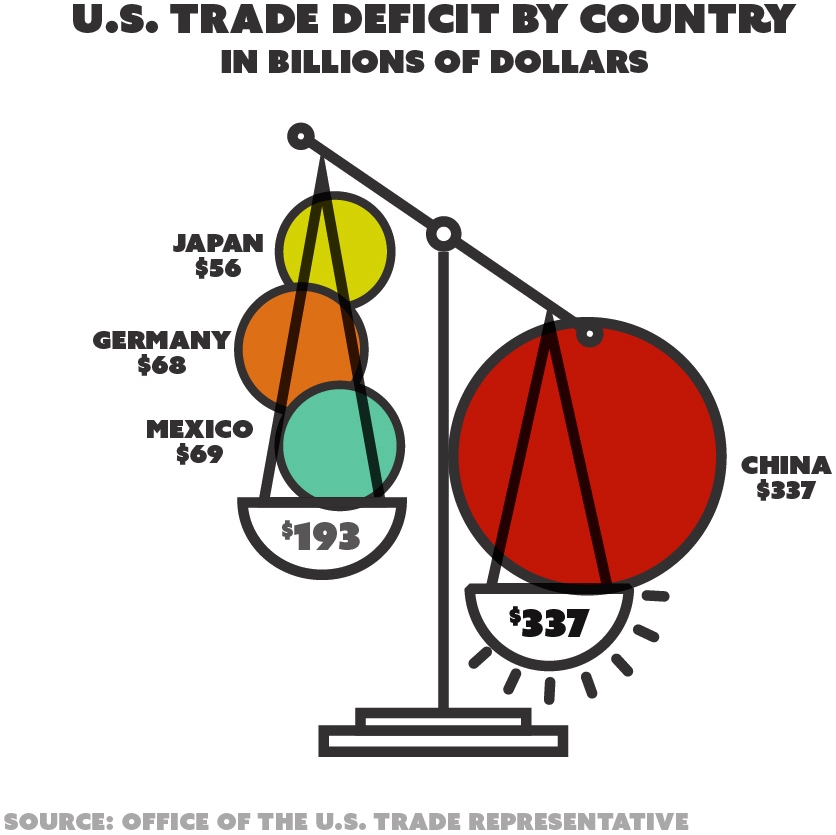

Few economic phrases sound more alarming than "trade deficit". It conjures images of a country living beyond its means, losing out to foreign rivals, draining wealth abroad. Politicians invoke it as proof of decline; headlines treat a widening deficit as bad news by default. The reality is more interesting and far less gloomy. A trade deficit is an accounting fact, not a verdict, and understanding what it does and does not tell you is one of the most useful things in economics. Here is what a trade deficit really is, why it is so widely misread, and how it fits into the bigger picture.

What it is

A trade deficit occurs when a country imports more goods and services than it exports over a given period. In other words, it buys more from the rest of the world than it sells to it. The opposite situation, exporting more than you import, is a trade surplus, and when the two are equal, trade is balanced.

The figure is usually reported as the trade balance: the value of exports minus the value of imports. If exports exceed imports, the balance is positive (a surplus); if imports exceed exports, it is negative (a deficit). It can be measured for goods alone, for services alone, or for both combined. This balance is one component of how international trade shapes a national economy, and it feeds directly into the way economists measure output.

Goods, services and the wider balance

A common mistake is to treat "trade" as meaning only physical goods, cars, machinery, food. But trade in services counts too, and for some countries it is enormous. Banking, insurance, consulting, education, tourism and software can all be sold across borders, even though nothing is shipped in a container.

This distinction matters a great deal for somewhere like the UK. Britain has long imported more goods than it exports, producing a goods deficit, while running a substantial surplus in services, where it sells more abroad than it buys. The overall trade position depends on combining the two.

The trade balance is itself part of something larger called the balance of payments, the full record of a country's economic transactions with the rest of the world. That includes not just trade but also income from investments abroad and flows of money in and out. A central insight follows from this: the balance of payments, taken as a whole, always balances.

Why a deficit always has a flip side

This is the part that surprises people. If a country is buying more from abroad than it sells, where does the money to pay for the extra imports come from? The answer is that a trade deficit is matched by an inflow of money on the other side of the books.

When foreigners sell goods to a country, they receive its currency. They do something with that money: they invest it back into the country, by buying its companies, its property, its shares or its government debt. So a trade deficit is mirrored by a capital inflow, foreign money flowing in to invest.

A trade deficit does not mean money is simply vanishing abroad. By definition, it is balanced by money coming back in as investment. The two sides are the same coin.

This is why economists say a deficit is "financed". A country running a persistent trade deficit is, in effect, attracting foreign capital. That can be perfectly sustainable, especially for an economy that foreigners are keen to invest in. It can also become risky if the country is relying on borrowing it may struggle to repay, which is the real question to ask.

Why a deficit is not automatically bad

Here lies the biggest misconception. A trade deficit is frequently treated as a sign of economic failure, but it often signals the opposite.

Consider what drives imports. When an economy is growing strongly, consumers have money to spend and businesses are investing, so they buy more, including more from abroad. A booming economy tends to suck in imports, which can widen the trade deficit. In that case, the deficit is a symptom of strength, not weakness. A recession, by contrast, can shrink a deficit as people stop buying, hardly a happy outcome.

Several other points temper the gloom:

- Imports are not a loss. They give consumers cheaper or better products and give businesses inputs they need. Buying foreign components can make domestic firms more competitive, not less.

- Currency adjusts. Exchange rates can move to make exports cheaper and imports dearer, helping to correct large imbalances over time.

- Investment is welcome. The capital inflow that finances a deficit can fund factories, infrastructure and jobs.

None of this means deficits never matter. A large deficit driven by weak exports and financed by unsustainable borrowing can be a genuine warning sign. The point is that the headline number alone tells you little. What matters is the why and the how: why the deficit exists, and whether the way it is financed can continue.

How it connects to the rest of the economy

The trade balance does not sit in isolation. Net trade, exports minus imports, is one of the components used to calculate a country's economic output, so changes in the deficit feed into the headline measures that policymakers watch. A swing in trade can nudge growth up or down.

It also interacts with currency markets, interest rates and investor confidence. A country seen as a safe, attractive place to invest can run a sizeable deficit comfortably, because money keeps flowing in. One that loses the confidence of investors may find a deficit much harder to sustain. This interplay between trade, investment and confidence is part of the same machinery that drives swings in financial markets, including the cycles described in a bull versus bear market.

| Term | What it means |

|---|---|

| Trade deficit | Imports exceed exports |

| Trade surplus | Exports exceed imports |

| Trade balance | Exports minus imports |

| Balance of payments | All transactions with the rest of the world |

The UK picture

The United Kingdom offers a clear, real-world illustration. For decades it has imported more goods than it has exported, running a persistent goods deficit, reflecting an economy that consumes a lot of manufactured products it does not make at home. At the same time, it has been a powerhouse in services, particularly financial and professional services, generating a surplus there that offsets part of the goods gap.

The Office for National Statistics, which compiles these figures, publishes the trade balance regularly, and it draws plenty of political attention. But the British case neatly shows why the headline goods deficit can mislead if read in isolation: it omits the services surplus and the investment flows that accompany the overall position.

The bottom line

A trade deficit simply means a country imports more than it exports over a period. It is one part of the balance of payments, and it is always matched by money flowing in the other way, typically foreign investment, so the books balance. Far from being an automatic sign of failure, a deficit can reflect a strong, growing economy whose people and firms are buying a lot, and imports themselves bring real benefits. The questions worth asking are why the deficit exists and whether it can be financed sustainably, not whether the number is negative. Treat a trade deficit as information to be interpreted, not a scoreline to be feared.

Frequently asked questions

What is a trade deficit in simple terms?

It is when a country imports more goods and services than it exports over a period. In money terms, more is flowing out to pay for foreign products than is coming in from sales abroad. The opposite, exporting more than you import, is a trade surplus.

Is a trade deficit bad for the economy?

Not necessarily. A deficit can simply reflect strong demand from consumers and businesses buying imported goods, often a sign of a healthy economy. Whether it is a problem depends on what is causing it and whether it can be financed sustainably over time.

How is a trade deficit paid for?

A trade deficit is matched on the other side of the books by inflows of money, such as foreign investment in a country's businesses, property or government debt. Because the overall balance of payments must balance, a deficit in trade is offset elsewhere.

Does the UK have a trade deficit?

The UK has run a deficit in trade in goods for many years, importing more physical products than it exports. This is partly offset by a surplus in services, including financial and professional services, where Britain sells more abroad than it buys.

Join in — free. Comments on Daily Junction are for members, so real names stay rare and bots stay out.

One field. We email you a 6-digit code — no password needed. Your comment is kept while you do it.

Under 13? You’ll need a parent’s OK first — it takes them one click.